The growth catalysts: Viewpoints from Indian OOH

By M4G Bureau - August 23, 2024

Leading voices of Indian OOH representing media owning firms shared their responses to 12 questions centred on the current business environment as well as the steps required to be taken for the industry’s growth and development. Outdoor Asia presents the findings of the survey, republished by Media4Growth.

NOW AND INTO THE FUTURE

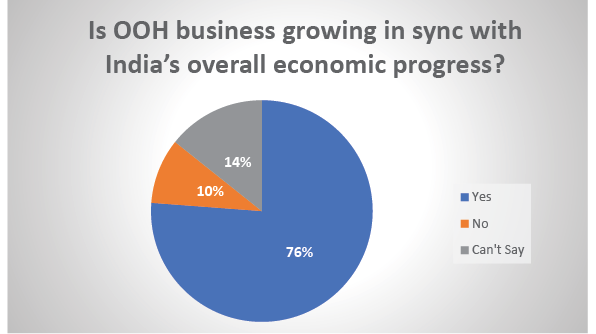

1. India will be the fastest growing national economy among all G-20 countries in 2024. India is also one of the fastest growing major economies, reports World Bank. Do you see Indian OOH business growing in sync with India’s overall economic progress?

A whopping 76% of the respondents took the view that India’s economic resurgence, and the fact that the country is among the fastest growing major economies in the world, is increasingly reflected in the progress of the Indian OOH business.

As such, India is the fastest-growing ad market globally and is projected to move into the top 10 markets in. Magna estimates the Indian ad market to grow at a CAGR of 10% to reach Rs. 1,70,000 crore (US$ 20.53 billion) by 2028. While this growth will be largely sustained by the digital media expansion, OOH is also expected to gain more traction in the short to medium term.

That said, nearly a quarter of the respondents to the survey have held some reservation of the country’s economic growth creating growth avenues for OOH, with 10% of the respondents categorically taking the view that the overall economic progress will not have a bearing on Indian OOH’s growth process.

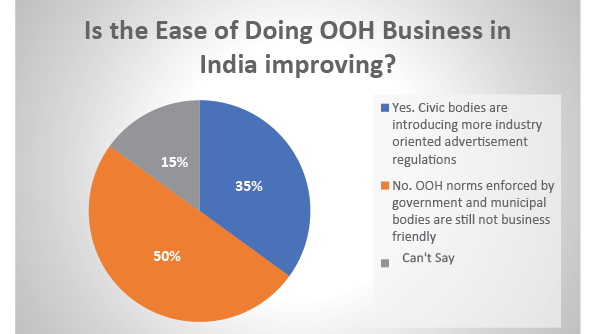

2. Is the Ease of Doing OOH Business in India improving with civic bodies implementing more media-ownership friendly advertisement regulations?

For any sector to draw more investments, it is imperative for the policy makers and regulators of that sector to establish an investor-friendly business environment. In the case of Indian OOH, and more particularly with respect to media owning business, the governing regulations are not seemingly consistent and that deters many business entities from making longer-term investments in this sector.

In this survey, only 50% of the respondents have maintained the view that the civic bodies in the country, who determine the local outdoor advertising norms, are ushering in regulations that augment the Ease of Doing OOH Business. The other 50% hold the view that the Ease of Doing Business is not at par with what is expected, with 35% of the respondents clearly stating that the Ease of Doing Business if not improving for the Indian OOH media owning business.

It may be noted that more recently, civic bodies in cities like Mumbai and Bengaluru are introducing new ad bylaws with the express purpose of ushering in standardised norms, stringent regulation of the media, as well as for augmenting their revenue inflows. The outcome of the new ad bylaws could have a major bearing on OOH regulation in several other cities.

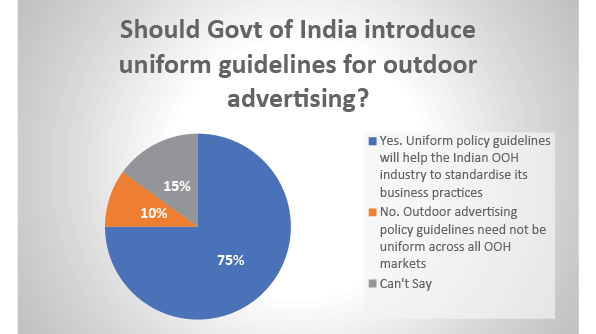

3. Should the Union Urban Development Ministry introduce uniform guidelines for outdoor advertising across the country?

One of the major challenges for media owning businesses that operate in multiple cities is the multiplicity of ad norms, and often conflicting provisions. Today, as various OOH media owning firms look to scale up their operations and invest in different regional markets, it is imperative that the ad norms governing OOH across the cities and towns are more standardised. In the past, the apex industry body Indian Outdoor Advertising Association (IOAA) had taken the initiative to recommend to the Union Urban Development Ministry the adoption and enforcement of a common code for outdoor advertising, by which certain standard guidelines would have been followed by the various OOH regulating bodies. However, that initiative has not seen the expected outcomes.

In this Survey, 75% of the respondents have taken the view that the Union Urban Development Ministry should look to introduce uniform guidelines for outdoor advertising across the country. Yet, a quarter of the respondents have not felt the need for uniform guidelines, with 10% of the respondents even taking the view that such uniform guidelines are not required for Indian OOH.

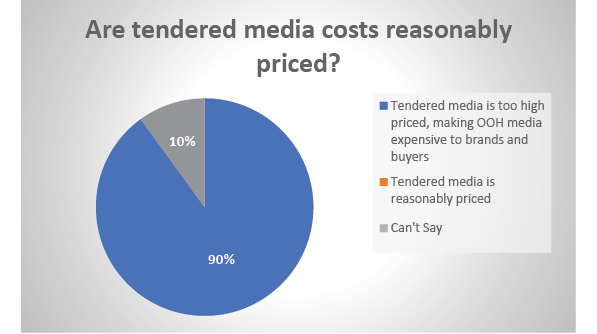

4. Are tendered media costs reasonably priced by municipal authorities and other government authorities that award advertising contracts?

While the Ease of Business is challenging for most media owners and operators across the country, several media owners have been particularly concerned over the rising tender costs of media. A high 90% of the respondents have taken the stand that tendered media costs are way too high, and not quite viable for investment. The high cost of media makes OOH an expensive medium for advertisers and media buyers, which is inimical to the growth prospects of OOH. As one media owner had stated in an interview with Media4Growth a few months ago that the authority wants the revenue but does nothing to help the outdoor media owners to do their business.

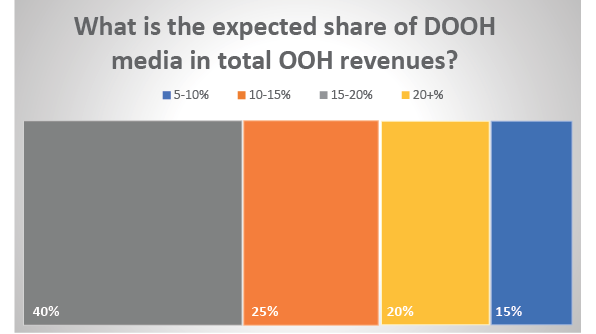

5. In the last 2-3 years, DOOH media has come up in significant ways in several cities across the country. In the next 3 years, what is the expected share of DOOH media in total OOH revenues?

The increasing pace of digitalisation of Indian OOH media is illustrative of the changing business landscape of this medium. Digitalisation is not only bringing with it greater efficiency and transparency in the advertising process, but also extends the boundaries of creativity, such as, use of anamorphic 3D displays. DOOH expansion also sets the ground for widescale use of programmatic platforms for media buying.

In this Survey, 40% of the respondents said they expect DOOH to account for 15-20% of total ad revenues within the next three years, which is a bullish outlook considering that current DOOH share is estimated at about 5%. Another 25% of the respondents believe that DOOH share of the total ad revenues in India will settle in the region of 10-15% in the next three years. Far smaller segment of the respondents expect the DOOH share to either clock upwards of 20% or at 5-10%. One may derive from the above stats that DOOH in India will broadly account for the upper end of the 10-20% range of total ad spends. However, if the pace of digitalisation is supported by enabling OOH ad norms across cities, this segment could even achieve 20+% share of the OOH ad pie, on the lines of the more evolved OOH markets in the West.

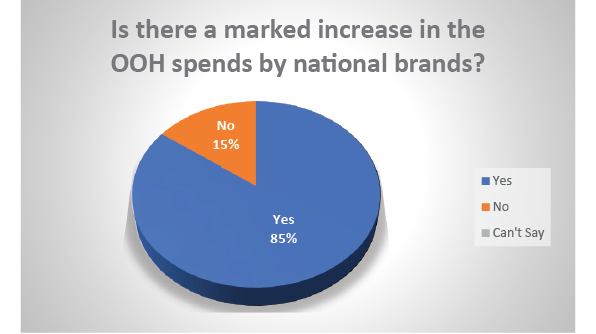

6. Based on business trends seen in the period 2022-24, do you see a marked increase in the OOH spends by national brands?

While OOH is used to a great extent for hyper-local marketing, various national brands have been using this medium very effectively by launching multi-city campaigns across regions. As such, for the national brands to apportion a great share of their ad budgets for OOH advertising, it is imperative for the OOH industry to come up with a common currency that assures total transparency, accountability and greater RoI on their spends. That said, various brands have been using OOH in highly creative ways, and making significant impacts on the audiences.

In this Survey, a sizeable 85% of the respondents have said that national brands are indeed stepping up their OOH spends, which is a hugely positive signal for the Indian OOH industry. 15% of the respondents have however taken the view that national brand spends on OOH is unlikely to increase from the current levels.

Today, as OOH embraces new technologies, and a much wider spectrum of formats are made available to the advertisers, there is an over-arching belief that the OOH growth has just begun and that a much wider pool of national brands will take the OOH route for their marketing and brand building efforts.

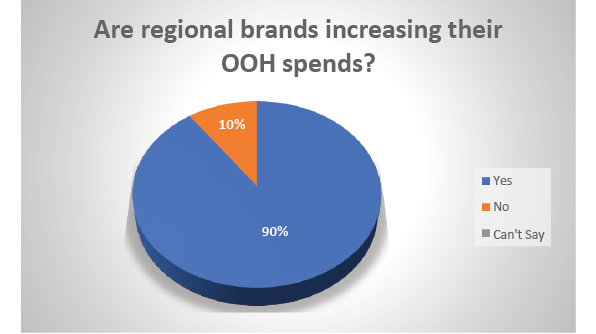

7. Are regional brands increasing their OOH spends?

Meanwhile, in keeping with the economic dynamism of the non-Metro cities, and the increasing pace of industrialisation of the cities and towns, regional brands are coming up in significant ways, each asserting their visible presence on the business turf. The ensuing competitive business environment has also sparked off more marketing initiatives by these brands, which is reflected in the number of regional brands that launch sizeable OOH campaigns.

In keeping with this trend, media owners expect the regional brands to also step up their OOH spends. 90% of the respondents to this Survey have maintained the view that regional brands will continue to increase their spends on OOH.

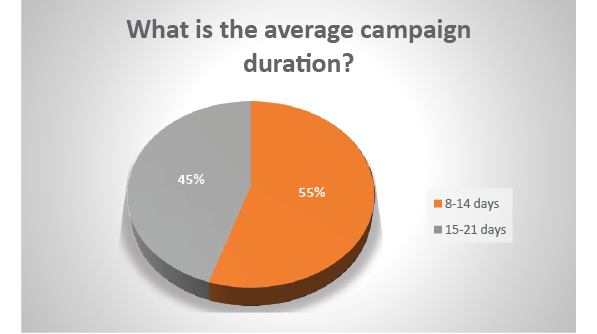

8. Drawn from your business experience in the last 3 years, what is the average duration of OOH campaigns?

There was a time when outdoor advertising campaigns ran for weeks and months, but all that changed in the last 10 years as the average campaign duration reduced drastically. This has hurt the media owners as the average occupancy rates went down. Time to time, the industry bodies have attempted to adopt a common practice wherein media owners are expected not to accept any campaign for display if the duration is below the generally agreed upon timeframe. But, that has not come through, given that the media ownership is highly fragmented and a common stance on the same may be difficult to arrive at.

What is evident from this Survey is that the majority (55%) of the respondents cite the average campaign duration at 8-14 days, and another 45% cite the average duration at 15-21 days.

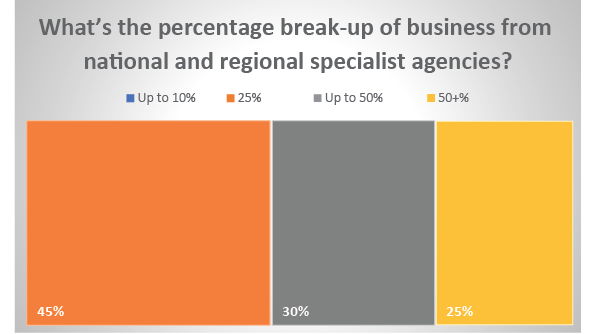

9. What percentage of business comes from national and regional specialist agencies?

While it has been cited that national and regional brands are expected to increase their OOH spends in the coming times, this Survey reveals that 45% of the respondents (media owners) expect 25% of their overall advertising business to come from the specialist agencies. 30% of the respondents expect up to 50% of their business to come from the specialist agencies, which is more likely the phenomenon in the major metro markets. Another 25% reckon that agencies will deliver over 50% of the total business that they do. Interestingly, none of the respondents cited share of business from specialist agencies to be less than 10% of their overall OOH advertising business.

It may be concluded that the percentage of business coming from the specialist agencies is on the high side in the larger OOH markets, and that the share comes down proportionately with the size of the OOH markets that are addressed. That said, many of the specialist agencies are recognising the importance of Tier 2 and 3 markets and are looking to combine conventional advertising with experiential activities to get the national and regional brands to use OOH in those markets.

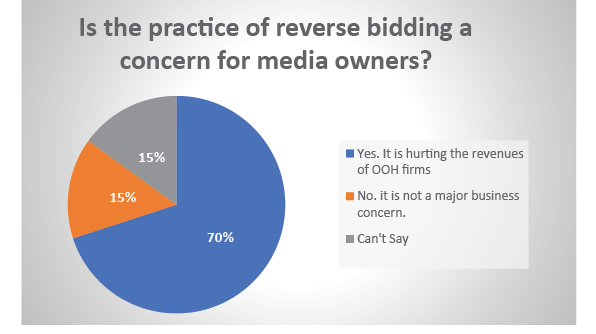

10. Is the practice of reverse bidding a concern for media owners?

The media owning industry has collectively recognised the opportunity to increase and perhaps double the OOH share of total ad revenues. This would be possible only if the total OOH revenues increase but in volume and value terms. That is, on one side the number of advertising using OOH must go up, but on the other side, the advertising yields should also increase as brands and buyers pay as per the defined media rates. But, the emerging realty suggests a different picture. Media owners not only face challenges such as having to provide volume discounts but they are also being subjected to the consequences of reverse bidding, which is severely commoditizing the medium as a whole. The apex body IOAA has time to time suggested the need for collective action to root out the reverse bidding practices.

This Survey shows that 70% of the respondents term reverse bidding as a major business concern for OOH media owners. 15% of the respondents have suggested that it does no harm to the media owning business, whereas another 15% did not offer a concrete view on this matter. However, as the overwhelming majority of the respondents have aired their concern over the practice of reverse bidding, it is imperative for the industry to come together as one and take down this practice.

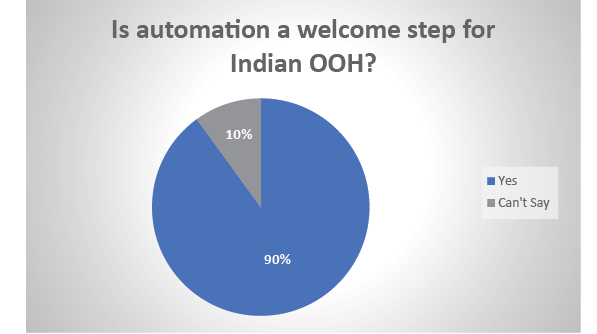

11. Is automation a welcome step for Indian OOH?

On a different plane, Indian OOH is seeing early signs of automation coming into the business, although there is very little evidence of that having impacted the trajectory of the business thus far. But, looking at the automation trends in the major OOH markets around the globe, the days of automation of OOH business is not too far. At the outset, automation is expected to bring in efficiency in the systems and processes, and all mundane activities will be conducted by machines, leaving the more intelligent and creative processes to be handled by trained manpower. Ocean Outdoor’s Stephen Joseph has shared his perspectives on this theme in a separate interview that is featured in this edition.

What’s most remarkable is that 90% of the respondents to this Survey have attested to the view that automation is a welcome step for the industry. Looking ahead, one can expect to see OOH firms across the board embracing automation and programmatic solutions.

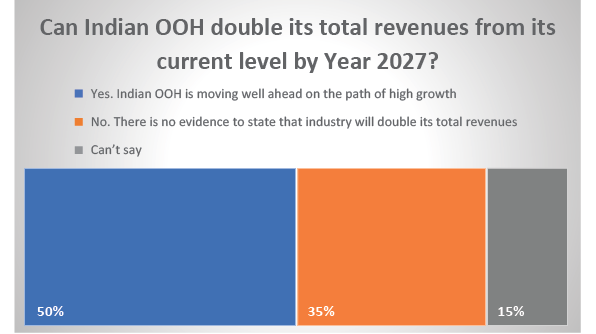

12. Do you expect Indian OOH to double its total revenues from its current level by Year 2027?

And, finally, on the question of whether Indian OOH can double its revenues in the next three years, 50% of the respondents have said an outright yes to the question, whereas another 15% were unsure if that can be achieved. However, a significant 35% of the respondents believe this goal cannot be achieved, although in this Survey we have not gone into the reasons that support the respondents’ responses to the questions.

Overall, it is amply evident from the Survey outcomes that the majority of Indian OOH media owners are optimistic of a significant uptrend in business in the foreseeable future, and they are open to embracing the latest technologies and practices that set the ground for accelerated business growth.

Stay on top of OOH media trends

_440_851.jpg)

_140_270.jpg)

_(1)_140_270.jpg)