Industry News

Indian advertising economy touches Rs1tn: Magna Global Ad Forecasts – Dec 2023 Update

India is now consistently the fastest growing market and leads the ad spend growth globally. India moves into top ten markets and forecast to climb to 8th position by 2028.

KEY FINDINGS

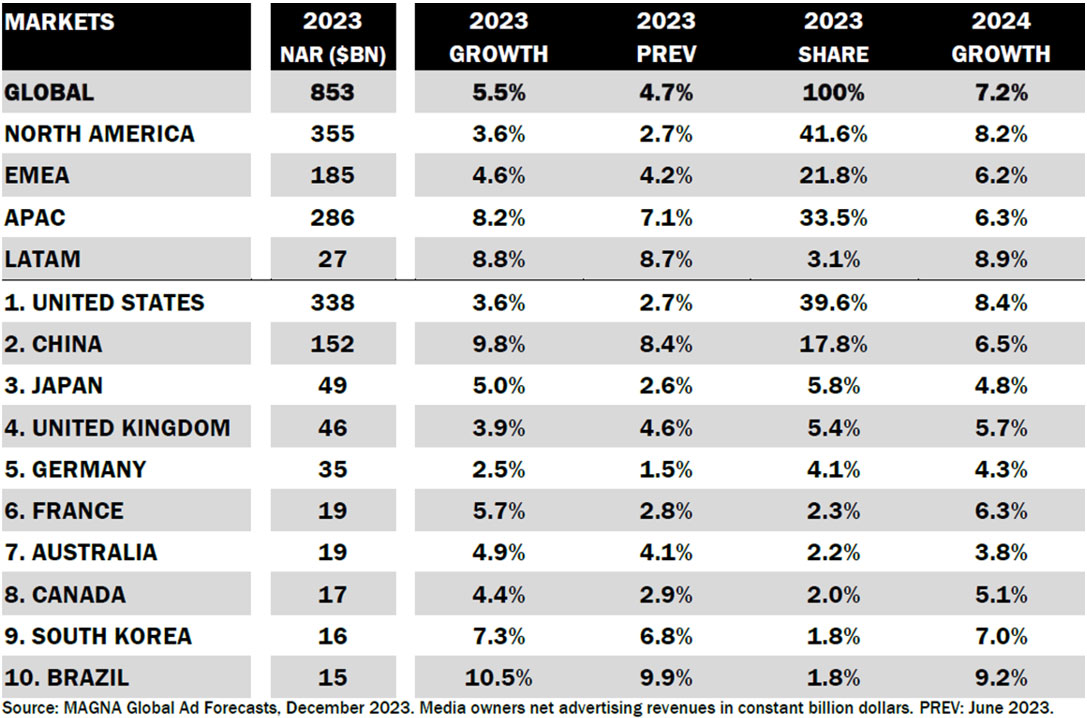

- The winter update of MAGNA’s “Global Ad Forecast” predicts that global media owners net advertising revenues (NAR) will reach $853bn this year, +5.5% above the 2022 level, and will grow by +7.2% in 2024.

- The Asia Pacific advertising economy grew +8.2% to $286bn this year powered by India, Pakistan and China. In 2024, APAC advertising revenues will increase +6%.

- India is now consistently the fastest growing market and leads the ad spend growth globally. India moves into top ten markets and forecast to climb to 8th position by 2028. Indian advertising sales grew +11.8% in 2023 to ₹1099bn ($14bn) and is the 11th largest market.

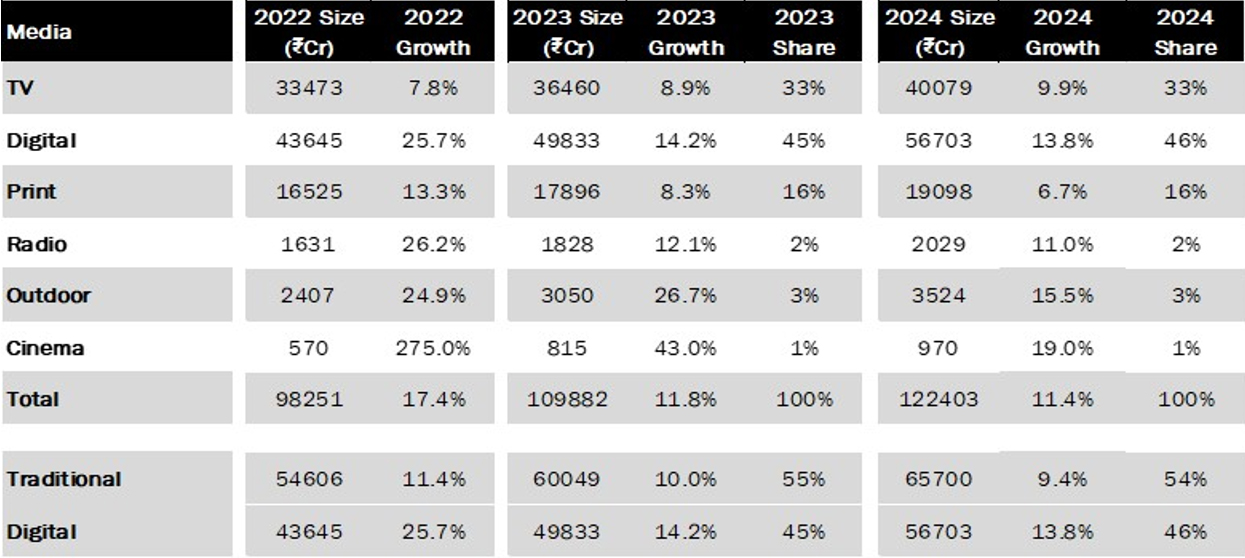

- In India, Digital formats contribution to growth is slowing down (+14.2% in 2023 Vs +25.7% in 2022), however digital remains the largest at INR 500bn ($6.4bn) with a share of 46%. Linear formats will grow by +9.9% with both Television and Print growing equally at +8%. Radio (+12.1%) and OOH (+29.8%) are seeing a robust recovery though still short of pre-COVID revenue.

- In 2024, the India advertising market will grow by +11.4%. Digital formats will rise +13.9% to reach INR 569bn ($7.2bn), while linear ad sales will increase by +9.3% to reach INR 655bn ($8.3bn).

Fig 1: Global Forecast

Venkatesh S, SVP, Director – Intelligence Practice, MAGNA India, said: “In 2023H1 advertising spend grew +9.6%, accelerated in the second half of 2023 to +13.8%. The recovery is driven by festive spending and marquee events like ICC WC and elections. Globally, Traditional media owners’ (TMO) ad revenue growth is slowing down, while in India both Linear (+9.9%) and Digital formats (+14.5%) are growing. Traditional formats will still be the largest, at least till 2027, though pure play digital is driving the adex. Non-linear formats (AVOD, Digital Newspaper, Podcasting & DOOH) of TMOs are growing steadily in double digits and contributes 5% to the total revenue of TMOs.”

India along with China projected to contribute about half of global GDP growth in 2023 & 2024. After a +7.3% expansion in 2022, the IMF in their latest October 2023 update predicts a slight deceleration in economic activity with real GDP growth of +6.3% in 2023. The GDP has been revised up by 0.4% from the April 2023 update as economic growth remains robust. India is reliant on its own domestic demand, private consumption, and investment spending for its growth. The overall sentiment is positive and upbeat though the market remains complex with local and global pressures. Large consumer base and aspirations of the young Indians works in its favour.

Fig 2: India ad revenues

Inflation remains vulnerable to rising food and fuel prices. The task of bringing inflation back to target is a priority for the government through macroprudential measures and monetary policy tightening. After a +6.7% in 2022, inflation though expected to ease down to +5.5% in 2023 is still in the upper bracket of the central bank’s desired range.

The Union Budget’s focus on boosting manufacturing, higher disposable income with lowering of taxes and increased spending on infrastructure augurs well for the adex growth. Advertising spending is growing at a healthy rate of +11.8% in 2023. Total ad sales are rising from INR 982bn ($12.5bn) in 2022 to INR 1099bn ($14bn) in 2023.

Consumers are increasing their spending, primarily driven by the young working adults who are investing in experiential led categories like travel, auto, entertainment. Impassable categories like CPG, continue to see higher spending. 2023H2 which includes festive spending, ICC World Cup and government spending before the upcoming national elections early next year is expected to contribute 10-12% incremental growth to adex.

CPG, auto and fintech are the most dominant sectors contributing to India’s adex growth followed by government, communication, travel, and real estate. Retail including e-commerce, financial services, Media & Entertainment and Apparel will see average growth, Startups who have been the main stay for all tent poles properties have either cut budgets or moved to performance marketing than brand marketing. With the new retrospective taxation policy on gaming, brands have exercised caution in spending.

In the last few years, the Government has fostered the digital ecosystem with inimitable assets like Aadhar, UPI & DigiLocker taking the digital public goods to a higher level. Also, driven by rising internet user base and affordable devices, currently 881mn have access to internet as of March 2023, according to TRAI. Government has also initiated labs to develop applications using 5G service to ramp up digital business services and this will have a rub off on the digital advertising economy. In 2023, overall digital ad spends will grow +14.2% to top INR 500bn ($6.4bn). India takes the lead in Mobile growth followed by US and Brazil according to a report by Adjust and it is a mobile first market. The share of Mobile within digital will touch 59% this year. There are 467mn Social users in the country and it has been the bellwether for digital growth with +19% growth. Total Video registers +16% growth. It is noteworthy that OTT players display robust growth trends driven by increased CTV subscribers, content choices and local language play. The OTT subscription estimated to be at 50mn this year. In 2024 total digital growth estimated at +13.9% to touch INR 569bn ($7.2bn).

Overall Television is growing but Pay TV is facing challenges from Free Dish, FTA channels and OTT in terms of subscriber base. Following the implementation of the amended New Tariff Order (NTO) 3.0 which allowed broadcasters to hike channel access price, subscribers have moved out of Pay TV being a price sensitive market. Despite this, Television is still the largest video medium with over 900 million viewers and daily viewing at 222 mins. In the light of rising consumption of short form content along with web series and availability of TV shows on OTT platforms, the time spent indicates TV is holding onto its audiences. The proposed broadcast bill extending its purview to include OTT, will help eliminate disparities to the advantage of Linear television. Also, there remains considerable growth opportunity for TV and advertisers are keen to cover the vast population of live audience. Television ad revenues in 2023 will grow +8.9% to reach an estimated INR 365bn ($4.6bn). In 2024 TV advertising estimated to grow +9.9% to reach INR 401bn ($5.1bn).

Newspaper has risen to be the most credible source of information. With 391mn copies (2021-22) circulated every day and language print taking the lead, the geographical spread and the audience size presents a massive marketing opportunity. The advertising growth is on the back of recovery in volumes; however, yield remains a challenge. In 2023, ad sales revenue will grow +8.1% to INR 175bn ($2.2bn). Growth expected to continue in 2024 to drive an increase of +9%, INR 187bn ($2.4bn).

Radio’s road to recovery has been a gradual one. Despite the volumes crossing pre-covid levels, yield has been a struggle though ad rates have flared up slightly. The industry is battling challenges of measurement limitations and audio streaming apps gaining user base. Radio players are offering airtime bundled with off air solutions to make up for the revenue. Government led allowance of news broadcast and increase in Government advertising rates will accelerate ad spends. Overall, advertising revenues are growing by +12.1% to reach INR 18bn ($229mn), which is 80% of the pre-COVID market size. In 2024, radio estimated to grow +11%, INR 20bn ($254mn)

OOH advertising has consistently grown post the pandemic as audience movement continues to ascend. Rising roadside DOOH screens in metros and state capitals, substantial presence in ambient spaces have added to demand, leading to growth in DOOH spends which contributes 5% to total. In 2023 OOH revenue increased by 26.7% valued at INR 30bn ($382mn) reaching 90% of the pre-COVID market size. This pace will be sustained for few more years and in 2024, OOH will exceed 2019 revenues adding +16% to the size.

In-cinema advertising is up sharply as audiences are flocking to cinemas. State-of-the-art technologies like IMAX and Dolby Atmos, has transformed movie-watching into a truly awe-inspiring experience and this has been another reason for audience draw. It will cover 74% of 2019 market size by the end of 2023 with an impressive +43% growth to reach INR 8bn ($102mn). In 2024, the growth is estimated to be +19%.

Hema Malik, Chief Investment Officer, IPG Mediabrands India, commented: “India continues to script its unique narrative in the advertising landscape, boasting robust growth across diverse mediums despite evolving consumer preferences and market dynamics. The promising trajectory across television, digital, radio, and out-of-home channels signifies the dynamic nature of our advertising landscape. I am optimistic about the future as India’s advertising story unfolds, driven by innovation, adaptability, and a burgeoning consumer base.”

Daily Newsletter

Subscribe to receive the latest OOH

industry updates

Being Human marks Salman Khan’s birthday with a bold OOH campaign

Redmi unveils bold multi-platform campaign for Note 14

CBC invites tenders for rent-free hoardings in Delhi

Bhavin Kothari, CIO of ace turtle, to address DDX Asia Business Conference

Skechers launches 3D cricket shoe Bus Shelters in Mumbai

“With digital content, you don’t have to wait for the product to be manufactured”

Ocean Outdoor collaborates with fashion designer & human rights activist Louise Xin to run DOOH broadcast in 6 countries

Pizza Hut drives brand visibility with OOH campaign in emerging markets

Zepto’s Fast 10 Minute Delivery Saves the Day for Game Night in Ahmedabad!

Unilever concludes global media mandate review with agency shifts across markets

‘Let’s create an empathetic space for women’

‘It won’t just be a man’s world anymore’

‘We’re actively exploring acquisitions and working to increase our inventory’

A habit of success at Prakash Arts

‘OOH is an important channel to connect with corporate audiences’

Operation Manager

Company Description: BajuGali an Advertisement Company is a leading firm specializing in advertising and marketing services. We provide innovative solutions...

Senior Copy Editor

No of openings: 1 Experience/ qualifications: 3-4 years in any media/news publication Graduate Degree in any discipline, degree in Journalism...

Sales Specialist at BajuGali (OOH Advertising Company)

At BajuGali, we are a marketing and advertising agency that specializes in transforming creative visions into reality for brands and...

Multiple Openings – Bright Outdoor Media (Business Development Manager, Admin & HR Manager, Sales Executive)

BRIGHT OUTDOOR MEDIA LIMITED SINCE 1980 JOB VACANCY: Business Development Manager (Media Selling Exp. is a must) Admin & HR...

Sales Executive – Street Furniture/Transport

Job description – Sales (Street Furniture/Transport) Location – Delhi, Mumbai, Chennai Designation & Compensation – Will depend on the candidate...

Sales Executive cum Coordinator, OOH Media

Key Responsibilities 1. Sales Execution Lead Generation and Prospecting Client Meetings and Presentations Sales Negotiation and Closing Reporting and Forecasting...

Business Head – OOH (South India)

ideacafe.agency is a new age dynamic through-the-line communication specialist agency. We’re seeking a Business Head OOH South to lead our...

Reporters/Content Writers

Job Type: Full Time Job Location: Bangalore

Netflix India goes full green light on OOH with Squid Game season 2

With pink guards, high-visibility hoardings, and metro and cab wraps in crowded spaces, Netflix India’s 360-degree OOH campaign ensures maximum...

Hafele launches innovative anamorphic billboard featuring Sachin Tendulkar

The campaign enhances consumer engagement, presenting Hafele’s home and lifestyle products as a must-have

Aditya Birla Sun Life Mutual Funds’ customer centric OOH Campaign

This campaign is executed by Interspace Communications

Bajaj Electricals’ 3D anamorphic OOH campaign in Bangalore

This campaign brings to life three of Bajaj’s flagship categories – water heaters and mixer grinders

Tata Capital’s ‘Mitaye Faasle’ OOH campaign

Tata Capital's 'Mitaye Faasle' campaign creatively leverages innovative ooh advertising to connect with audiences and bring dreams closer to reality.

Revolutionising campaign management: Praphul Misra on the future of Digital Signage

Praphul Misra discusses how Oi Media is revolutionizing advertising workflows with tools like IAQT and IBXD, which streamline campaign management,...

“Our strength lies in innovation and scale”

Shubham Kumar, Managing Director, Dinesh Plastic Works emphasizes on their innovation, large-scale production capacity, and adaptability to client needs.

Navigating the LED display market: Expert tips for quality and efficiency

Gangasagar Amula, Managing Director of Absen India, highlights the need for clarity in selecting LED displays. He stresses prioritizing energy...

Coca-Cola presents virtual snow globes in immersive AI DOOH experience

The interactive DOOH artwork was created for Coca Cola by Ocean and appears between 3pm and 6pm until Christmas Day.

“From P10 to P6, and now to P4, we’ve come a long way”

Ajay Mody, Owner of Alliance Signotech, sheds light on the evolving landscape of DOOH advertising, from advanced technologies to the...

-

Campaigns

CampaignsNetflix India goes full green light on OOH with Squid Game season 2

-

Creative Concepts

Creative ConceptsSkechers launches 3D cricket shoe Bus Shelters in Mumbai

-

Campaigns

CampaignsBeing Human marks Salman Khan’s birthday with a bold OOH campaign

-

Sustainability

SustainabilityStatus of sustainable printing in the OOH Industry: Challenges and pathways forward